Complaint Statistics

March 2026

In this edition we present the complaints statistics for the first half year of 2025.

Explanation of Complaint Categories

Conduct – refers to complaints arising from the process in which insurance is sold, the handling of client’s premiums or monies, cross-border selling, unlicensed selling, allegations of fraud, allegations of forgery of insurance related documents, commission rebates and “twisting” (i.e. insurance agents inducing their clients to replace their existing policies with those issued by another insurer by misrepresentation, fraudulent or unethical means).

Representation of Information – refers to complaints relating to the presentation of an insurance product’s features, policy terms and conditions, premium payment terms or returns on investment, dividend or bonus shown on benefit illustrations, etc.

Claims – refers to complaints in relation to insurance claims. The IA cannot adjudicate insurance claims or order payment of compensation. It can, however, handle complaints related to the process by which claims are handled (e.g. delays in processing, lack of controls or weaknesses in governance, areas of inefficiency in the claims handling process).

Business or Operations – refers to complaints related to business or operations of an insurer or insurance intermediary, (for example, cancellation or renewal of policy, adjustment of premium, underwriting decision, or matters related to the management of the insurer, etc.).

Services – refers to complaints regarding insurance related servicing by insurers or intermediaries, such as complaints related to the delivery of premium notice or annual statement, dissatisfaction with services standards etc.

Overall Complaint Trend

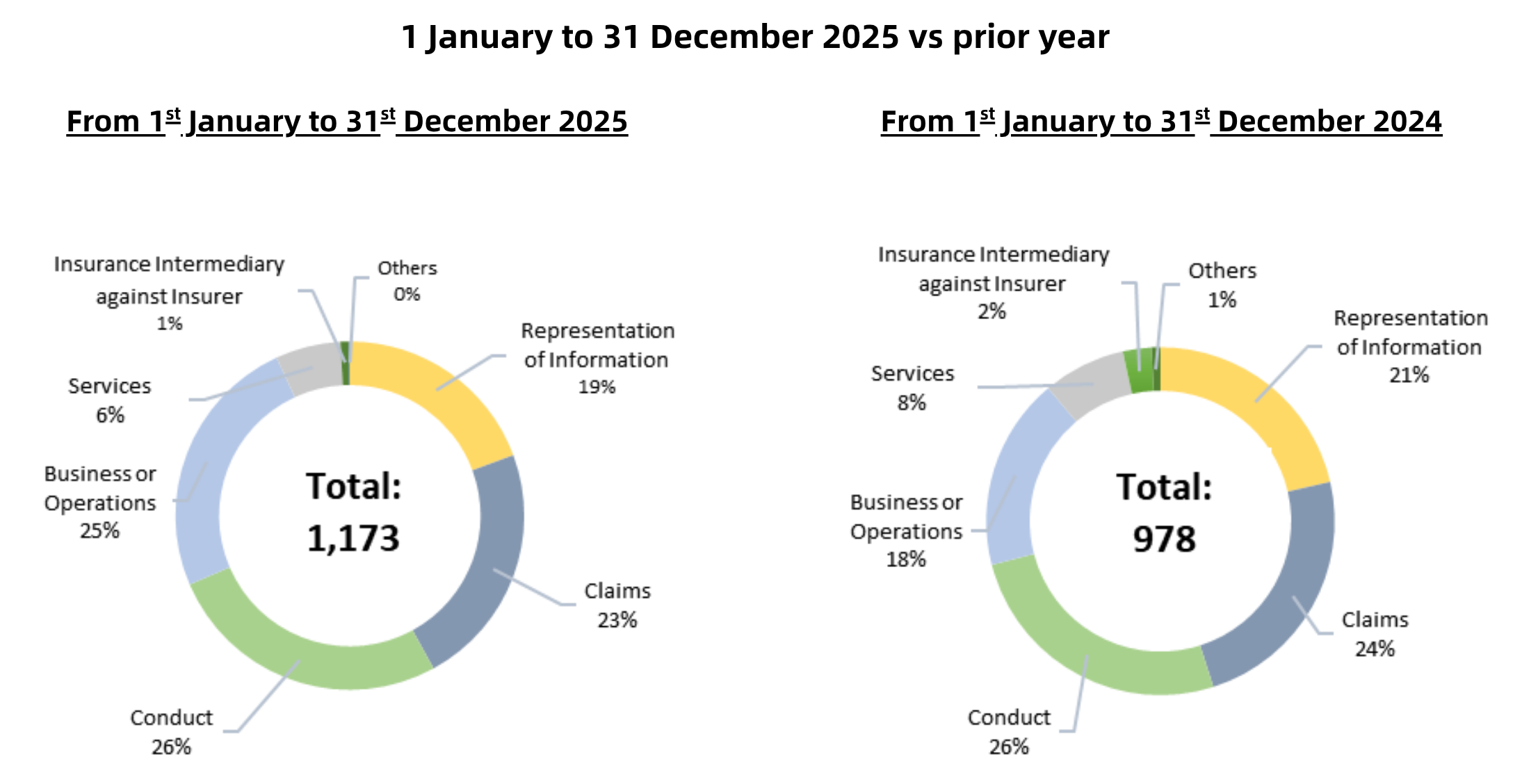

In 2025, the IA received 1,173 complaints, representing a 19.9% increase from the 978 complaints recorded in 2024. In the first half of 2025, the year-on-year increase hit 33% but dropped in the second half to reach the final of around 20% figure for the full year.

Despite the increase in 2025, the overall complaint volume remained broadly in line with pre-COVID levels of 1,163 complaints in 2019, and was 21% lower than the pandemic-period of 1,494 complaints in 2020. In the context of the insurance market’s continued expansion (in only the first three quarters of 2025, total gross premiums hit HKD637 billion, far exceeding the full year figure of HKD567 billion for 2019), the complaint trend has been relatively moderate.

Alongside the observed complaint trends, the IA continued to enhance the efficiency of its complaint handling. In 2025, the IA exceeded its service pledge to close at least 80% of complaint cases within six months of receipt1, by achieving a six-month closure rate of 85% for complaints received during the first half of the year. This reflects our ongoing efforts to process cases efficiently while ensuring that outcomes are reached in a fair and consistent manner.

Complaint Profile and Regulatory Response

Looking more closely at complaint categories, “Conduct” (26%), “Representation of Information” (19%), and “Business or Operations” (25%) remained the major categories in 2025.

The significant increase in “Business or Operations” was discussed in the previous edition of Conduct in Focus (see Issue 11) covering the complaint statistics for the first half of 2025, and the observations set out there remain applicable when assessing the full-year position.

“Conduct” and “Representation of Information” together accounted for 45% of all complaints. Complaints in these two categories are, to a significant extent, associated with insurance intermediary behavior, including pre-contract sales practices and ongoing servicing provided after policy inception. This concentration underscores the importance of ensuring that intermediary incentives remain well aligned with policy holder interests and support consistently good customer outcomes throughout the policy lifecycle.

Against this backdrop, the IA has introduced commission spreading requirements for all participating policies with regular premium payment terms, as of 1 January 2026. This requires insurers to spread commission over the course of the policy period such that no more than 70% of the total commission can be paid within the first year, with the remaining portion being spread evenly over the following five years or the premium payment term, whichever is shorter.

The requirement applies to participating policies because they represent a significant segment of the long-term insurance market, accounting for more than 80% of new office premium, and because commission arrangements for these products have consistently been predominantly front-loaded. Where commission on a participating policy is all paid up front, it results in over-prioritization of selling (sharpening the risk of aggressive selling and miss-selling) whilst also underprioritizing post-sales servicing. Requiring commission to be more spread over the course of the policy period helps address this misalignment, incentivizing appropriate advice, quality sales activities, and meaningful ongoing services. Over time, the IA expects this measure to help ameliorate certain key drivers underlying complaints relating to conduct and misrepresentation of information, and support more sustainable market practices and better consumer outcomes.

In addition to commission-related measures, the IA has continued in recent years to place emphasis on the continuing professional development (“CPD”) training requirement. This reflects the IA’s expectation that insurance intermediaries should, through ongoing training, remain properly equipped with sound business ethics and up-to-date technical knowledge to serve customers effectively. The IA is pleased to note that the industry achieved a 99.9% CPD compliance rate, again, for the latest assessment period from 1 August 2024 to 31 July 2025. This outcome reflects the industry’s strong commitment to maintaining professional standards (whilst also leaving 0.1% room for improvement next year).

Notes:

1 Begins from the date on which written consent and supporting documents were received from the complainant to the date on which a referral was made to the Enforcement Division or the Conduct Supervision Division for follow-up action, or the date on which a letter of conclusion was issued to the complainant.