Insurance Intermediary Trends at a Glance - Age, Turnover and Licence Duration

March 2026

Age Statistics

In Issue 8 of Conduct in Focus (Issue 8), we shared the age statistics of insurance intermediaries up to October 2023. Two years on, we can continue to examine the trend up to December 2025.

Overall Trend

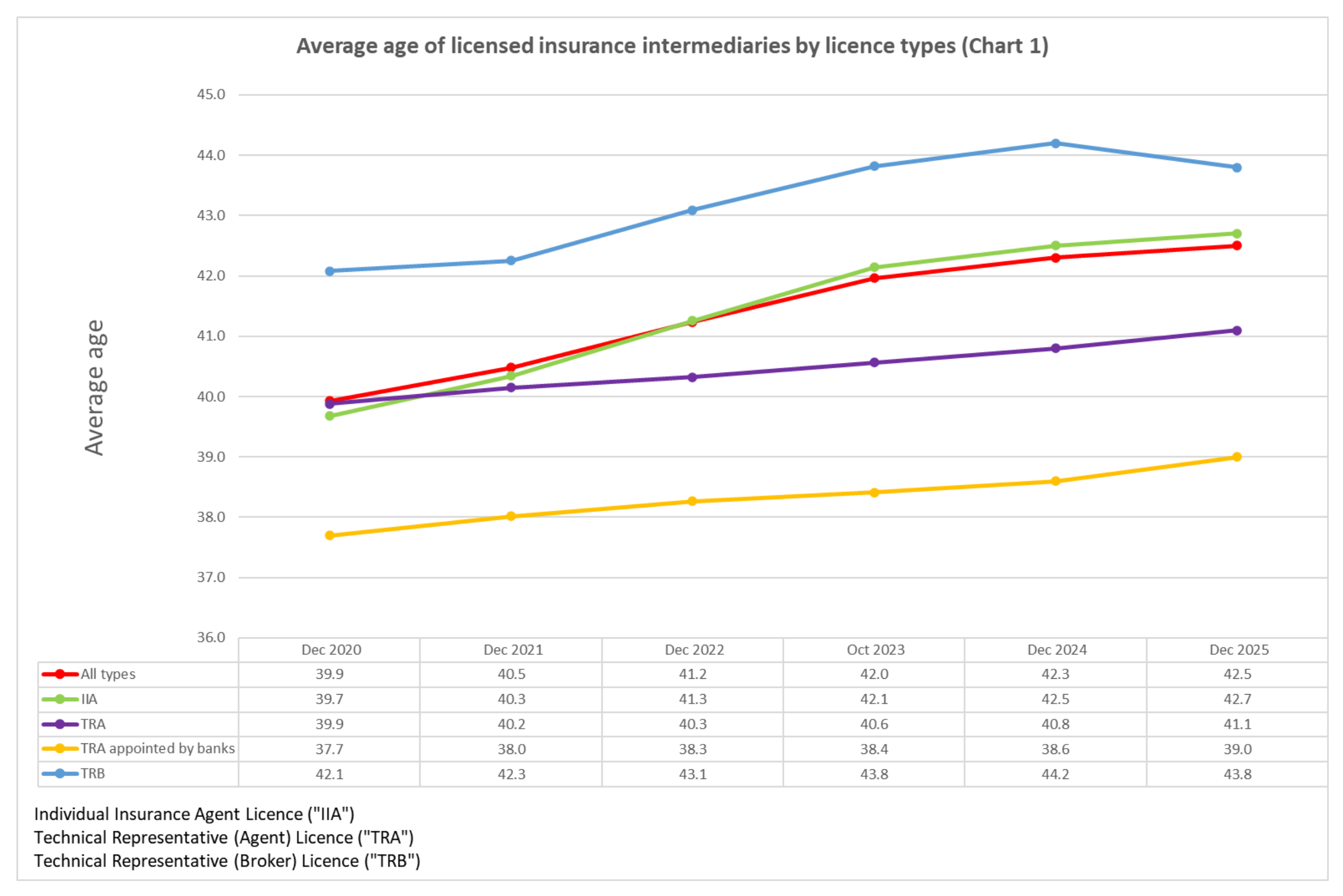

Overall, the average age of insurance intermediaries continues to trend upwards. In December 2020, it stood at 39.9 years. It then climbed steadily past the 40-year barrier to 42.0 years old as at October 2023. By December 2025, the average age had risen further to 42.5 years old.

Still increasing, then, but the slower pace may suggest signs of positivity. The fact that the average rose by only 0.5 years over a 2-year period (October 2023 to December 2025) indicates that inflows of younger entrants are – to some extent - counterbalancing the natural ageing of intermediaries already in the industry. This was different from previous years. Is this a sign that talent sourcing (particularly young talent sourcing) is beginning to stabilize?

Average Age Across Licence Type

Chart 1 details the progression in average age by licence type from December 2020 to December 2025.

Age Ranges

With an average age of 43.8 years, technical representatives (broker) continue to be the most (how should we put this) mature cohort among all licence types. However, this was unchanged from October 2023, suggesting that the broker segment has witnessed an injection of younger entrants in the past two years. By contrast, the average age of individual insurance agents increased from 42.1 years in October 2023 to 42.7 years in December 2025 (+0.6).

Similarly, the average age of technical representatives (agent) climbed from 40.6 years in October 2023 to 41.1 years in December 2025 (+0.5). Despite this increase, they remain the youngest group among all licence types, largely due to the relatively youthful technical representatives (agent) in banks, whose average age is lower at 39.0 as of December 2025 (+0.6).

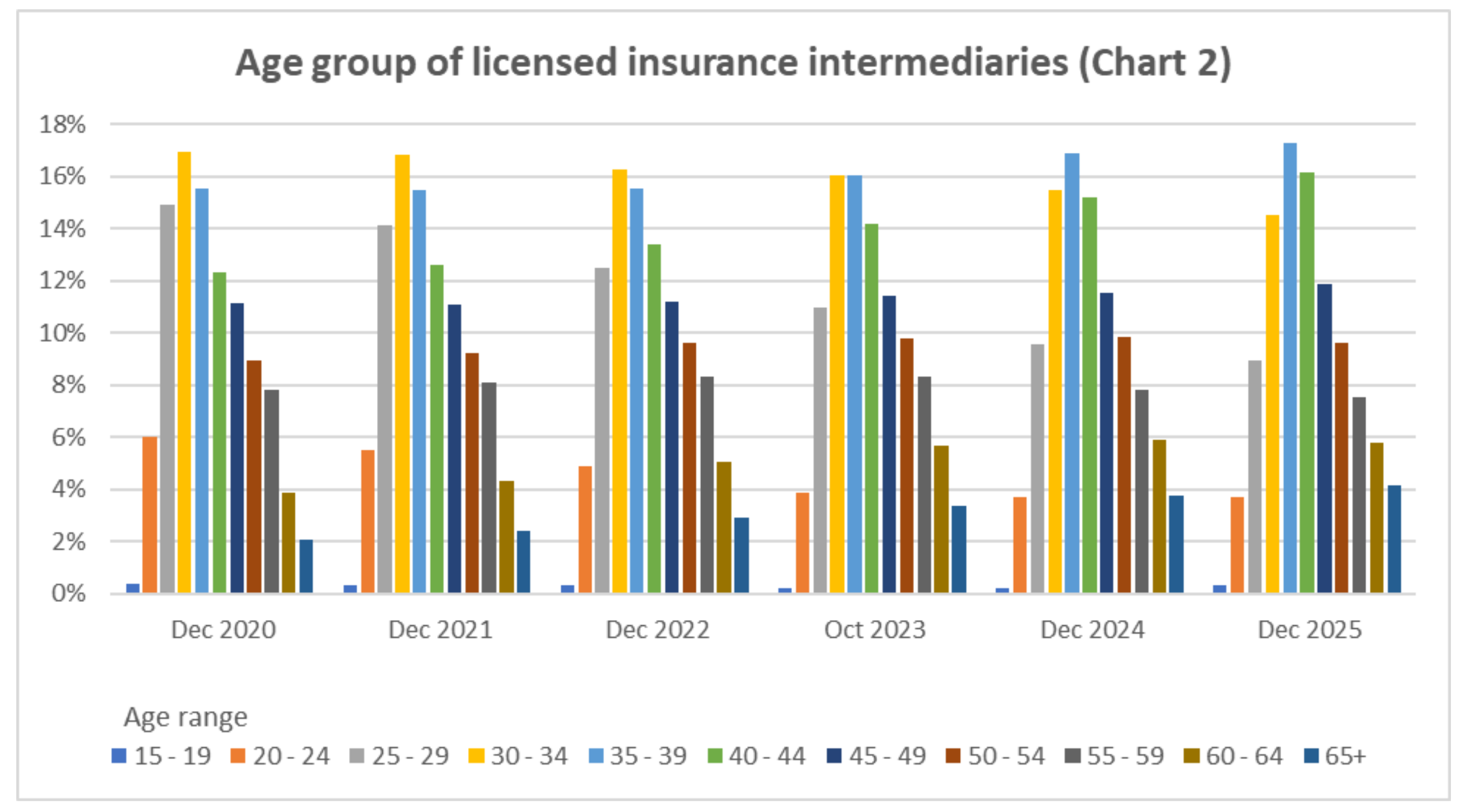

In Chart 2, we break down all licensed individual insurance intermediaries into 5 year age-ranges.

Here we see a change. The age group of 30-34 year olds was the largest from December 2020 to October 2023. By December 2025, this age-group dropped to the third largest, overtaken by the 35-39 and 40-44 age groups. The 25–29 age group has also fallen to 9% in December 2025, from 15% in 2020.

Turnover Rate

In issue 10 of Conduct in Focus, we showed the statistics for turnover rates among licensed insurance intermediaries up to 31 December 2024. Let’s explore how this continues to trend up to December 2025..

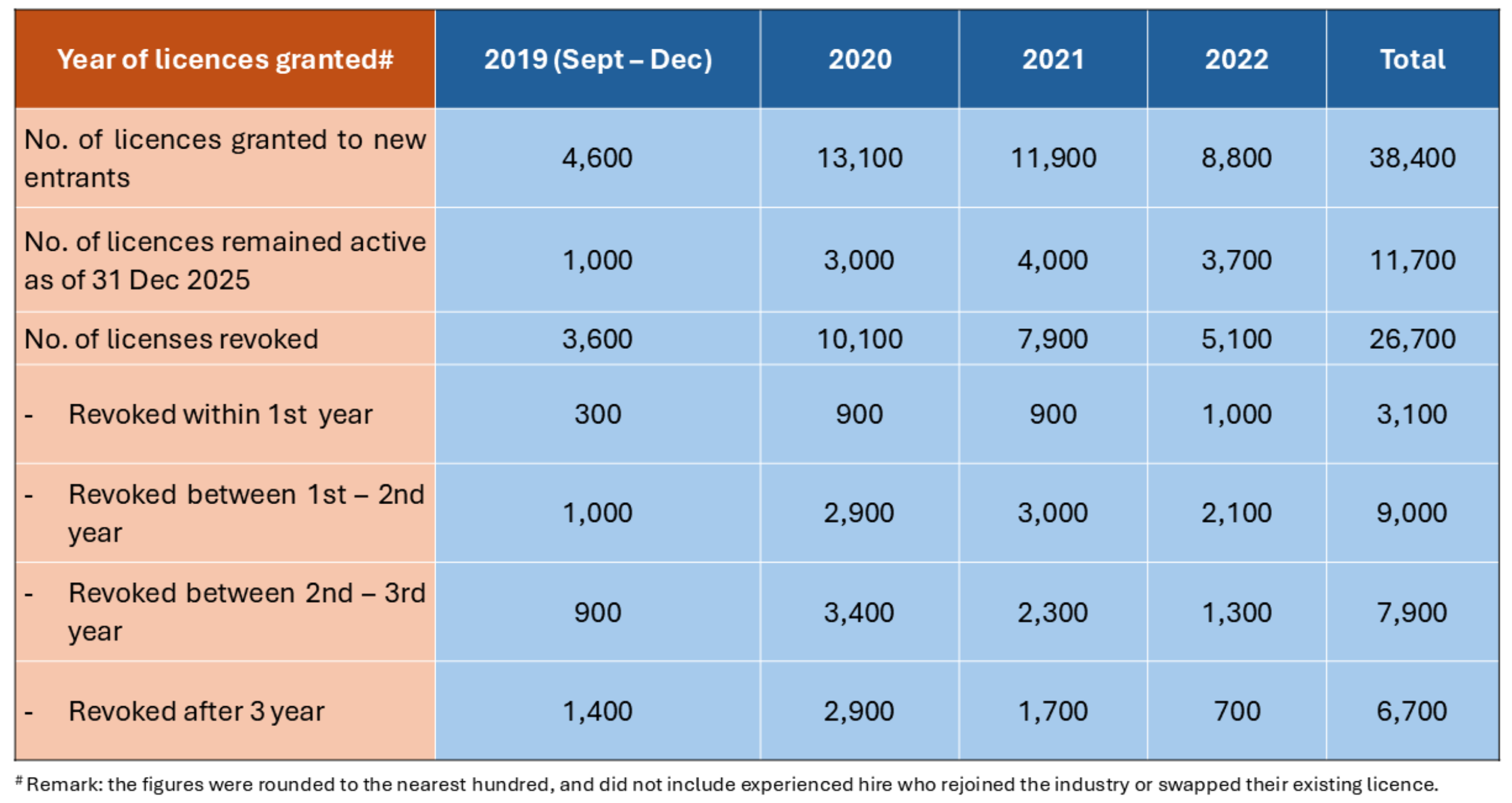

Of the approximate 90,000 individual licensees granted to new entrants to the insurance market from September 2019 to December 2025 (the life span of the IA’s licensing regime), around 53,000 (59%) continued to be active as at December 2025, down from 62% at the end of 2024.

That overall figure, however, only tells part of the story.

The picture is more telling when we focus on individuals whose licences were newly granted between September 2019 and December 2022, as they would by now have completed their first three-year licence period - allowing us to see how many actually renewed their licences (i.e. remained active in the industry).

- From September 2019 to December 2022, the IA issued 38,400 new licences to individuals entering the market for the first time.

- Of these, only around 30%, or around 11,700, remain licensed more than three years later, as at December 2025.

- This represents a further (considerable) decline from the 35% retention rate reported last year.

The data also indicates persistently high early‑stage attrition: in both periods reviewed, more than 50% of new licences were revoked within the first three years. Below are the key statistics for these new entrants:

From a conduct‑regulatory perspective, these figures continue to present a significant red flag, particularly regarding the risk of orphan policies in the life insurance sector. Orphan policies remain a key driver of complaints received by the IA, and persistently high attrition among new licensees heightens this concern. The data further reinforces the rationale for introducing the commission‑spreading mechanism for participating policies, which helps mitigate conduct risks arising from rapid turnover in the intermediary population.

Licence Duration in Individual Applications

Given the persistently high turnover among new entrants, it is also important to examine how licensees are choosing their licence duration options, as this may reflect their expectations of career longevity within the industry.

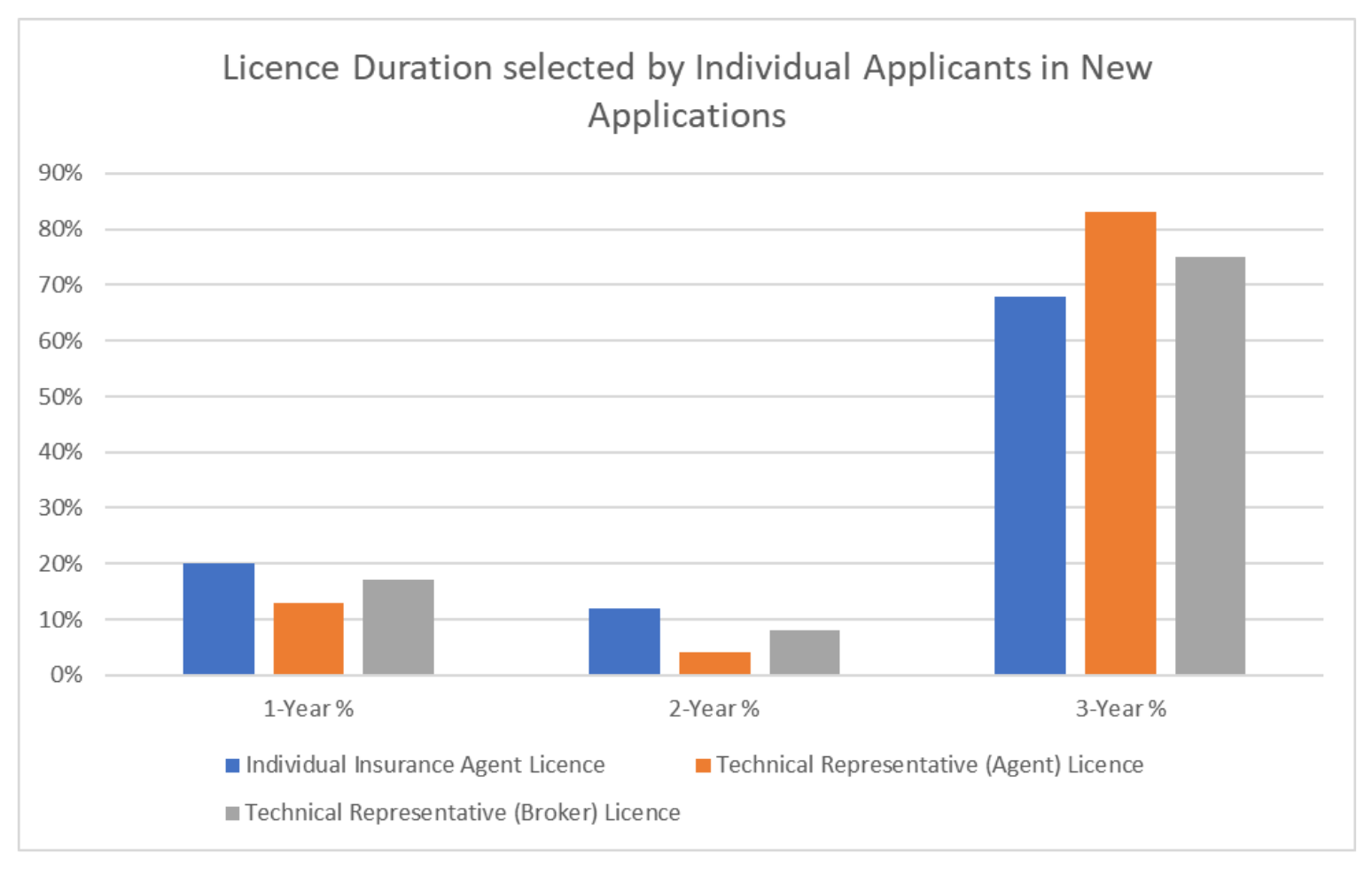

With the commencement of the licensing fee collection on 23 September 2024, new individual applicants have been offered the options to select shorter licence terms of 1 or 2 years, alongside the standard 3‑year term, at correspondingly lower fees. While the 3‑year licence carries a higher total fee, it offers a lower annualised cost. The aim of this flexibility is to reduce financial pressure on applicants and support new talents entering the market. Renewal applicants are likewise given the option of a 2‑year term in addition to the 3‑year licence.

Given the relatively high turnover rate shown above, one might expect applicants to choose shorter licence periods. However, the data reveals the opposite trend.

Despite higher total costs, 3‑year licences continue to be the preferred option, chosen by 71% of the approximate 31,000 new individual applicants from September 2024 to December 2025, showing their commitment to longer careers in the insurance market. Technical representatives (agent) led with 83% picking 3 years, followed by technical representatives (brokers) at 75% and individual insurance agents at 68%. Only 19% of the applicants during the period chose 1-year term.

Meanwhile, among the around 22,000 renewal applications received from September 2024 to December 2025, 84% selected a 3‑year licence while 16% chose a 2‑year option. This suggests that applicants who have completed their initial licence period tend to opt for a longer-term commitment.

Even though 3‑year licences require a higher upfront payment, their lower per‑year cost led most intermediaries to choose the longer term. This behaviour enhances policy holder protection by encouraging sustained intermediary availability and relationship continuity.

The current trend, with 71% of applicants selecting 3‑year licences, points to higher initial commitment.

However, as mentioned above, historical records show that 52% of past cohorts did not maintain their licences for the full three years. We are therefore keen to assess whether this strong initial preference reflects a real shift toward longer‑term commitment, or whether it is primarily driven by the lower annualized cost of the 3‑year option.

Final Comments

Our suspicion is that embedded with these statistics - particularly the 52% of licencees who fail to complete their first 3-year licence - is the persistence of the traditional distribution mindset. This mindset is based on the simple formula of “the more intermediary the better” – which lends itself to indiscriminate volume recruiting to meet recruitment quota targets. The consequence of this is a large drop out rate – 52% - in the first few years.

One day, perhaps, a recruiting principal may do something radical and adopt a recruitment formula which says “the fewer but more committed and well-trained intermediaries, the better for sustainable business”. This would require a more discerning and targeted approach to recruitment.

Some may say that in a world where every commentator is talking of how AI is going to disrupt traditional business models, there is something reassuring in the persistence of the Hong Kong traditional intermediary mindset. Having said that, as next article on the public perception of licensed insurance intermediaries demonstrates, perhaps a recruitment strategy that places more emphasis on quality than just sheer quantity, will lead over time to an enhancement of the positive perceptions and an eradication of the negative?

The IA, having introducing commission spreading requirements for participating policies, has no doubt that insurance intermediaries should be incentivized to see a career as an insurance intermediary as a long term commitment (and continue to earn tail commission as they service the policies they arranged). We hope that long-term insurers follow this lead.