Promoting Insurance on Social Media

March 2026

It is not unknown for the Insurance Authority (“IA”) to receive complaints about the manner in which an insurance intermediary or insurer promotes insurance products on social media. Sometimes, it doesn’t even take a complaint – just the vigilant eyes of an (often younger) IA staff member who has seen a misleading post come up on their feed. When that happens, usually we call the person responsible, tell them to stop being stupid and take the post down (and if they don’t, disciplinary action is the result). Occasionally, we will also pose as a potential customer, follow the link in post and see what other obvious non-compliances the person posting has committed.

The IA has not promulgated a series of detailed and granular rules specific to posting on social media about insurance, as we seek to preserve market flexibility and creativity. Rather, we rely on insurance intermediaries and insurers – should they choose to promote insurance via social media – to abide by the core conduct principles set out in section 90 of the Insurance Ordinance, on which the insurance regulatory regime for regulated activities is founded. In this article, to provide guidance, we show how these conduct principles apply - and are factored into the IA’s considerations - in relation to social media posts on insurance. We also give examples of the type of obvious non-compliances we have come across, so that these can be avoided in the future.

Applicable Conduct Requirements

The conduct requirements in section 90 of the IO which are most pertinent to social media use, are outlined below:

- An insurance intermediary should act in the client’s best interests, honestly, with integrity and treat the client fairly (section 90(a) of the IO).

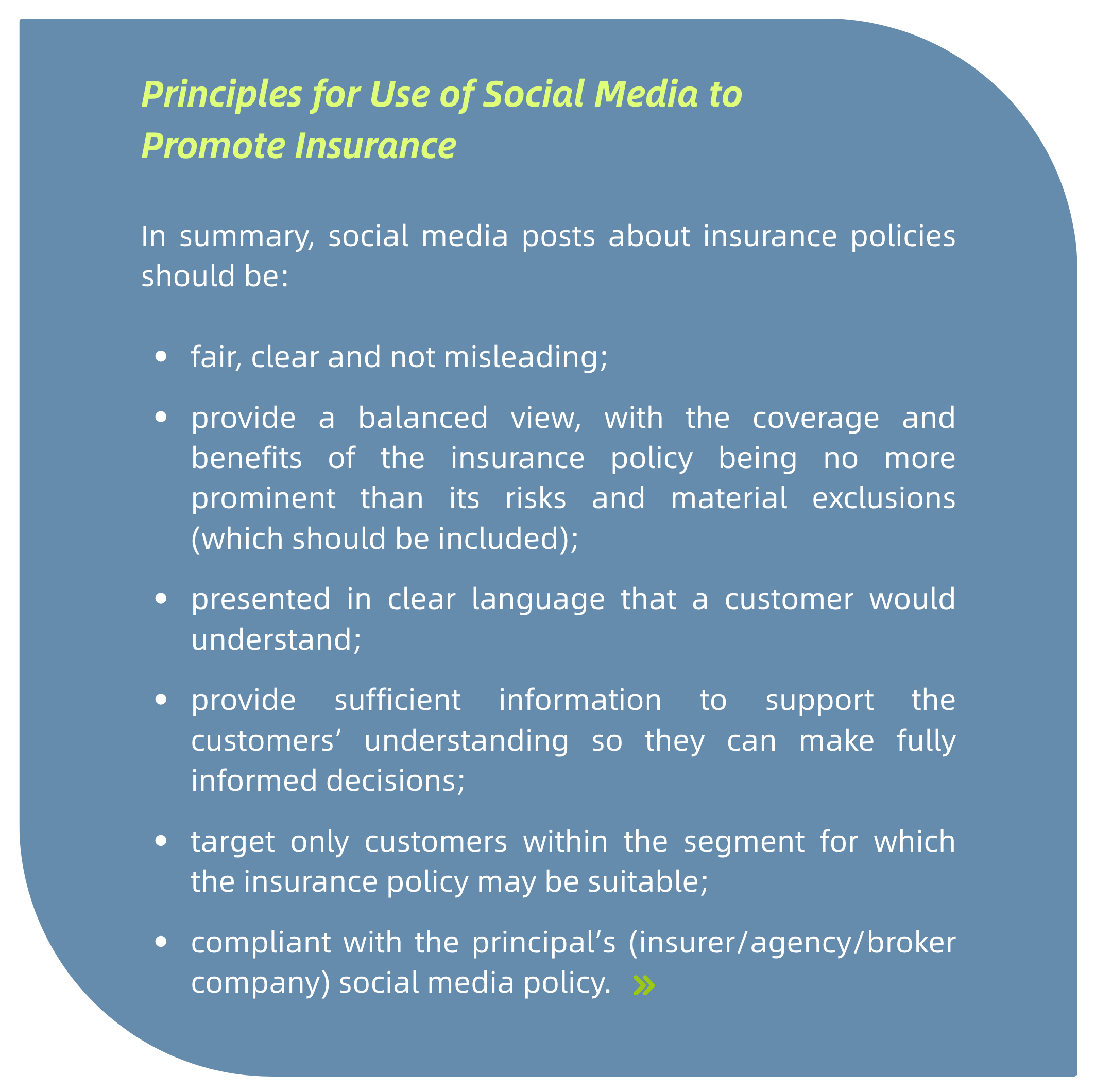

To accord with this conduct requirement when posting about insurance products on social media, it is imperative that the post is fair, clear and not misleading. This requires a balanced view of the insurance product to be presented, with the coverage and benefits of the insurance policy being no more prominent than its risks and material exclusions (which should be stated). The information should also be presented in clear language that a customer would understand.

- An insurance intermediary must disclose information about an insurance policy, for the customer to be sufficiently informed for the purpose of making an informed decision (section 90(e) of the IO)

This is the ultimate objective of regulated activities. Not to convince the customer to buy at all costs. But to provide the customer with sufficient information so they can make a fully informed decision. The aim must be to support a customer’s understanding, rather than getting them over the line on a sale as quickly as possible through distraction.

- An insurance intermediary’s regulated advice should be suitable for the customer, taking account of the customer’s circumstances

Social media posts can often be targeted on specific demographics or persons indicating certain interests through their own social media usage. In crafting a targeting strategy, an insurance intermediary or insurer curating a post must seek to target only potential customers who would likely be within the target customer segment for which the insurance policy was designed.

- Adequacy of Systems and Controls

Sections 91 and 92 of the IO require licensed insurance broker companies and licensed insurance agencies to establish and maintain proper controls and procedures for securing compliance with the conduct requirements by their technical representatives.

Similarly, per General Principle 1 of the Code of Conduct for Licensed Insurance Agents, individual insurance agents are required to comply with the policies and procedures and other applicable requirements of their appointing insurers in relation to carrying our regulated activities. Authorized insurers are required to establish such policies and procedures as part of their intermediary management function, aimed at ensuring, among other matters, that the conduct requirements in the IO are complied with.

All principals (whether insurers, broker company or agencies) should therefore have in place a policy on the use of social media by their individual agents or their technical representatives. To the extent such use is permitted, they should also ensure appropriate controls and processes are in place so that proposed posts are published in compliance with the conduct requirements.

The IA’s Approach

When a social media post about an insurance policy comes across the IA’s radar screen, we follow three broad principles in our approach to reviewing it.

- Firstly, we review it to see if it aligns with the conduct requirements summarized above.

- Secondly, in performing this review, we look at the social media post as if we were a customer (in line with the IA’s core function to protect the interests of policy holders and potential policy holders and the public interest, it is only right that we step into their shoes and see matters through their eyes).

-

Thirdly, we expect each social media post to be standalone compliant with the conduct requirements. We would not expect, for example, a consumer to be presented in a post with the benefits of the product, but have to click through to another post to see its drawbacks and risks. This would not be a fair or balanced presentation of the insurance policy.

The Type of Posts to Avoid

Probably the most common types of problematic social media posts we see are those which do not present the insurance policy in a fair or balanced way. Instead – and this is often the case with participating policies with non-guaranteed benefits – the post focuses on a prominent non-guaranteed benefit to “hook” the attention of the scrollers.

These days it is called ‘clickbait’, but it is a sales trick as old as time. A graph which shows the non-guaranteed benefit multiplying tenfold+ over a period of time, as compared with a bank deposit. A prominently highlighted percentage showing the return on non-guaranteed benefits a customer could enjoy, with the associated risks either hardly visible or not referenced in the post at all. A high percentage fulfilment ratio placed prominently in the post, where the percentage has been selected from the first or second year of the insurance policy to make any consumer’s eyes light up – even though this is totally misleading because of the fulfilment ratios it omits from later years.

When we catch the promoter in the act, out comes the pre-rehearsed defence – “ah, but of course, after they contact me, I will explain all the risks in full.” Sure you will. But the point is, you have already planted the misleading impression in the customer’s head, that they are virtually guaranteed to get the same return on the benefit shown in the post. You have created this misleading expectation. Psychologically, it is not easy to dislodge that thought once it has taken hold – which let’s face, was your objective in making such a misleading, unbalanced and unfair post in the first place. In these circumstances, the chances of a fully informed objective decision being made by the customer are very limited.

Another twist on the same sales-tactic, is the testimonial from the poster of how wonderful the insurance policy has been because he bought it himself. Here the poster is playing on ”social proof”, the idea that a consumer decides what is good for them based on what other consumers have bought. But here’s the problem – we are not all the same. Our insurance needs depend on our own individual circumstances and it’s the core task of an insurance intermediary to assess those circumstances and let the recommendation emerge from that. What’s good for you, may not necessarily be good for me. To suggest otherwise is potentially misleading.

Then there are those posts which promise a free iPhone if you buy an insurance policy. Whoever wrote these obviously hasn’t read the IA’s Guideline on Gifts, or deployed simple common sense. This is selling by distraction and it is not conducive to customers making informed decisions about their insurance needs.

Conclusion

Some obvious practical tips emerge from these observations.

- Social Media Policy: First, every insurer, broker company and agency should have in place a social media policy. This may be as simply as a straightforward prohibition on individual agents and technical representatives promoting insurance via social media. Alternatively, if such promotion is permitted, proper guidance should be provided (e.g. clear Dos and Don’ts and a formal approval process for product-specific social media posts) so that posts are properly controlled, with adequate record keeping to support audit and compliance needs.

- Communication Process: If you allow social media to be used, make sure your social media policy and guidance are clearly communicated to your individual agents and technical representatives. They should also be reminded to assess proposed post against the social media principles outlined in this article. Always remember that every post should be assessed on a standalone basis and consider it from the customer’s viewpoint.

- Be realistic: The fact is some insurance policies are too complex to be properly promoted in a balanced way through social media. It is perfectly acceptable to reach this conclusion and be discerning in your social media policy – permitting social media promotion for some types of insurance policies, but prohibiting it for others. A risk-based approach should be adopted in your considerations.

- Keep an eye out: There are tools you can use to carry out social media scraping and keep an eye on posts regarding your products and/or your company. It is a bit like mystery shopping, but with a compliance aspect. This is highly recommended.

- If in doubt don’t promote: It’s important to get it right, so if you’re in any doubt then not using social media to promote an insurance product would be the right decision. Because you never know, the customer who contacts you…could be working for us.